UPI Lite vs Regular UPI: Confused between UPI Lite and Regular UPI? This detailed guide explains the difference between UPI Lite vs Regular UPI, features, limits, benefits, security, charges, and best use cases. Updated for 2025 with tables, FAQs, eligibility and expert comparison

UPI Lite vs Regular UPI: What’s the Difference?

For updates and community discussions: Join our Telegram • WhatsApp: 7905455959 • Website: FinbankingTech.com

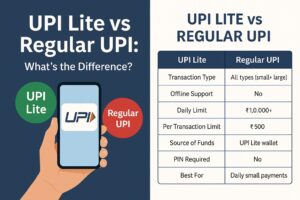

| Feature | UPI Lite | Regular UPI |

|---|---|---|

| Transaction type | Small-value payments (micro) | All bank transfers (small to large) |

| Offline support | Yes (limited) | No |

| Daily limit | ₹2,000 (NPCI guideline) | ₹1,00,000+ (bank dependent) |

| Per transaction limit | ₹500 | ₹1–2 lakh (bank dependent) |

| Source of funds | On-device UPI Lite balance | Linked bank account |

| PIN required | No (device auth) | Yes (UPI PIN) |

| Best for | Groceries, milk, recharges | Bills, merchant payments, high-value transfers |

Important Links

| NPCI UPI guidelines | npci.org.in |

| RBI circulars & updates | rbi.org.in |

| FinbankingTech — Official | finbankingtech.com |

| Join Telegram | https://t.me/FinbankingTech |

| WhatsApp Contact | +91 79054 55959 |

Eligibility Criteria

- Active bank account linked with your mobile number

- UPI-enabled mobile app that supports UPI Lite (latest version)

- Debit card linked during UPI registration (one-time requirement)

- Smartphone with basic security (screen lock/biometric)

- For UPI Lite: initial on-device wallet top-up (min. ₹200 recommended)

How UPI Lite Works (Simple Explanation)

UPI Lite operates like a tiny, in-app wallet inside your UPI app. You top up the wallet from your bank account once and then make multiple small payments directly from that wallet — often without entering a UPI PIN. This reduces dependency on bank servers and cuts failures during peak loads.

Top technical points

- Transactions may be routed off-ledger (device/local) and later reconciled with the bank.

- Device authentication or secure elements protect the balance.

- Limits are enforced by NPCI and individual apps/banks.

How Regular UPI Works (Quick Recap)

Every Regular UPI transaction is an authenticated bank-to-bank transfer (IMPS rails). You enter the UPI PIN (or biometric on some apps) and the payment is authorised and settled in near real-time through NPCI. Regular UPI supports QR payments, merchant on-boarding, autopay, billers, refunds and large-value transfers depending on bank limits.

UPI Lite vs Regular UPI — Detailed Comparison

| Parameter | UPI Lite | Regular UPI |

|---|---|---|

| PIN usage | Not required (device auth) | Required (UPI PIN) |

| Offline mode | Supported (limited) | Not supported |

| Acceptance | Small merchants & micro use-cases | All merchants & billers |

| Speed | Faster for micro-payments | Fast |

| Refunds | May not support full refunds | Full refund & dispute resolution |

What is UPI Lite? Features, Benefits & Working Mechanism

1. Key Features of UPI Lite

- Works even in weak or no network

- No UPI PIN required

- Stores up to ₹2,000 in a separate UPI Lite balance

- Instant, quick payments

2. How UPI Lite Works

UPI Lite works like a mini-wallet inside your UPI app. You load money → spend → reload whenever needed. Transactions are processed off-bank ledger, reducing load on bank servers.

What is Regular UPI? Full Explanation

1. Key Features of Regular UPI

- Direct bank-to-bank transfer

- Requires UPI PIN

- Works for large payments

- Supports QR, contacts, bill payments, subscriptions

2. How Regular UPI Works

Every time you send money, UPI authenticates using your UPI PIN and completes the transfer through IMPS infrastructure.

UPI Lite vs Regular UPI: Detailed Comparison Table

| Parameter | UPI Lite | Regular UPI |

|---|---|---|

| PIN Usage | Not required | Mandatory |

| Ideal For | Small, quick payments | All payments |

| Fraud Risk | Very low | Moderate |

| Bank Server Load | Low | High |

| FD, RD, Bills | Not allowed | Allowed |

| Merchant Support | Limited | Extensive |

UPI Lite Benefits (Why You Should Use It)

- Works faster than normal UPI

- Reduced failed transactions

- Works in offline mode

- No need to enter PIN

- Perfect for small daily payments

Regular UPI Benefits (Why It Still Matters)

- Complete payment solution

- High-value transfers allowed

- Best for online shopping, bills, and businesses

- Automatic refunds supported

- Widely accepted across India

When Should You Use UPI Lite?

Use UPI Lite when:

- You make many small payments

- Your area has weak mobile network

- You want secure, PIN-less payments

- You prefer fewer SMS alerts

When Should You Use Regular UPI?

Use Regular UPI when:

- You pay large amounts

- You need bank-to-bank transfer

- You make merchant payments

- You need detailed transaction records

- Is UPI Lite Safe? Security Explained

- Yes. UPI Lite is secured with:

- Device-level authentication

- NPCI’s offline ledger

- Limited spending power (₹500 per transaction)

- No PIN entry, reducing phishing attacks

Pros & Cons Table – UPI Lite

| Pros | Cons |

|---|---|

| Fast & offline-friendly | Limited to ₹500 per payment |

| No PIN needed | Not accepted everywhere |

| Low fraud risk | Wallet top-up required |

Pros & Cons Table – Regular UPI

| Pros | Cons |

|---|---|

| Accepted everywhere | PIN required every time |

| High-value payments | Failed transactions during server load |

| All bill payments supported | Slightly slower |

- Banks Supporting UPI Lite (2025 Updated)

- SBI

- HDFC

- ICICI

- Paytm Payments Bank

- Kotak Bank

- Axis Bank

- Yes Bank

- Federal Bank

- (More banks joining soon)

- Which One Should You Choose? Final Expert Recommendation

- For daily micro-transactions → Choose UPI Lite

- For regular banking payments → Choose Regular UPI

- Smart users can use both, depending on payment type

Who Should Use UPI Lite?

If you make frequent small purchases (tea, milk, local vendor), live in low-network areas, or want PIN-less convenience for routine spends — enable UPI Lite. It’s especially useful for households and micro-merchants who need quick turnarounds.

Who Should Stick to Regular UPI?

Use Regular UPI for bill payments, rent, merchant purchases, refunds, and any transaction requiring bank-level settlement or higher limits. Businesses and e-commerce sellers should continue to rely on Regular UPI rails.

Banks and Apps Supporting UPI Lite (Selected — 2025)

Major banks and UPI apps rolled out UPI Lite in 2024–25. Examples include SBI, HDFC, ICICI, Axis, Kotak, Paytm Payments Bank and Google Pay (app dependent). Check your app’s latest release notes to confirm support.

Practical Examples & Use Cases

Buying morning tea from a local stall (₹20–₹60) — UPI Lite

Paying electricity or mobile bill (₹800–₹3,000) — Regular UPI

Auto-recharge of transport card with low balance — UPI Lite for repeated small amounts

Safety & Security — What You Must Know

Both systems are governed by NPCI standards. UPI Lite reduces phishing risk since you don’t enter a PIN for every small payment; however, device-level security (screen lock, biometrics) is critical. Regular UPI uses PIN-based authentication and offers stronger bank-level dispute mechanisms.

FAQ — Quick Answers

Q1: What is the main difference between UPI Lite and Regular UPI?

- A1: UPI Lite is intended for micro, offline-friendly payments using an on-device balance; Regular UPI is full bank-to-bank transfers requiring UPI PIN.

Q2: Is UPI Lite safe?

- A2: Yes — it reduces PIN exposure by design and limits the value per transaction, lowering fraud impact. Still maintain device security.

Q3: Can I use both UPI Lite and Regular UPI?

- A3: Yes, most users will be able to use both depending on the payment scenario.

Q4: What is the per transaction limit for UPI Lite?

- A4: Typically ₹500 per transaction (NPCI guidance). Check your app for exact values.

Q5: What is the daily limit for UPI Lite?

- A5: Usually ₹2,000 per day (may vary slightly by bank/app).

Q6: Does UPI Lite require internet?

- A6: UPI Lite supports limited offline functionality in some implementations; most use online mode for reconciliation.

Q7: Can I get refunds on UPI Lite?

- A7: Refund support is limited and depends on the merchant/app integration; Regular UPI has more robust refund processes.

Q8: Will UPI Lite replace Regular UPI?

- A8: No. UPI Lite complements Regular UPI by handling micro-payments more efficiently.

Q9: Is UPI Lite free to use?

- A9: Yes — NPCI policy intends UPI Lite transactions to be free for end-users.

Q10: Can businesses accept UPI Lite payments?

- A10: Small merchants can accept UPI Lite if their app/QR supports it; widespread merchant acceptance may take time.

Q11: Do all banks support UPI Lite?

- A11: Not all banks initially — adoption is growing across major banks and fintech apps in 2024–25.

Q12: Is KYC needed for UPI Lite?

- A12: No separate KYC; existing bank KYC suffices.

Q13: Can I top-up UPI Lite from any linked bank account?

- A13: Yes, via your UPI app; top-up process depends on the app UI.

Q14: Which is better for frequent small spends?

- A14: UPI Lite — designed for frequent micro-transactions.

Q15: Will transactions show in my bank statement?

- A15: Regular UPI transactions show directly; UPI Lite transactions may reconcile periodically and reflect in statements differently depending on bank/app.

Q16: Can I send money to another person’s bank using UPI Lite?

- A16: No — UPI Lite is generally for payments to merchants or vendors, not bank transfers to third parties.

Q17: Does using UPI Lite affect cashback offers?

- A17: Cashback depends on merchant and app offers; some offers may be app-specific and differ for UPI Lite.

Q18: Can I deactivate UPI Lite?

- A18: Yes — disable or clear the UPI Lite balance from your app settings if you don’t want to use it.

Q19: Are there transaction charges for merchants?

- A19: Merchant charges are governed by NPCI and bank policies; many small transactions remain free or low-cost for merchants.

Q20: How do I know if my app supports UPI Lite?

- A20: Check the app’s update notes or payments section; most UPI apps show a “UPI Lite” option in wallet/payments settings.

Want This Post As A Printable PDF or WordPress-Ready File?

If you’d like, we can export this article into a WordPress HTML file, a downloadable PDF, or generate a featured image and an infographic for social sharing. Contact us: Telegram • WhatsApp: 79054 55959.

⭐ Conclusion

UPI Lite and Regular UPI both play a crucial role in India’s digital payment ecosystem. While UPI Lite simplifies small-value transactions, Regular UPI continues to lead in full-scale banking transactions. The right choice depends entirely on your daily usage and payment habits.

Debit Card vs Credit Card: Meaning, Difference, Pros & Cons

ITR Kaise Bhare? Step-by-Step ITR Filing Guide Online (2025)

No-Fee Bank Accounts : What They Are & How to Find the Best Ones